Q3 2024 Market Update: Bull Market Run Continues

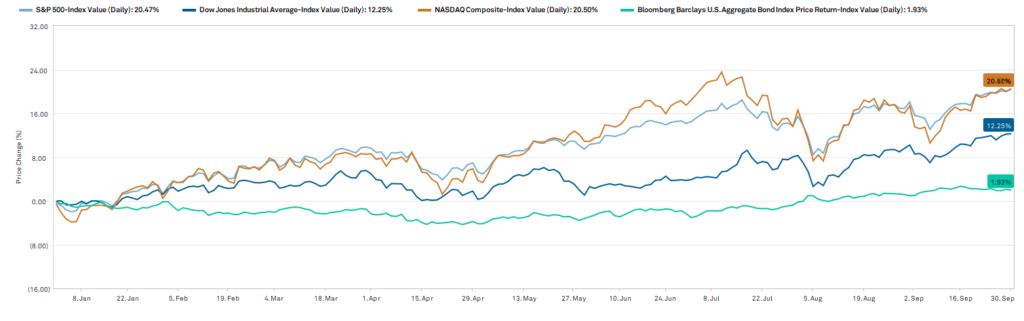

We’ve had a strong market this year, although it doesn’t quite feel like it. Both the S&P 500 Index and the Nasdaq Composite Index are up nearly 21% through September 30, 2024, and the usually stodgy Dow Jones Industrial Index is up a strong 12%. These are blockbuster returns – “normal” equity market returns are typically nearer 5-8%, with the post-financial crisis 10% annual rate considered higher than average. We have seen incredible strength in equities. The bond market is stable to slightly positive, with the Barclays Aggregate up nearly 2% year-to-date.

Macroeconomic factors remain the key drivers of market performance, as investors have all become “Fed-watchers”, anxiously anticipating for the Federal Reserve Bank’s (the “Fed”) next interest rate action. Despite the substantial year-to-date returns, there is the sense that the strength can be over in an instant.

This may be too gloomy, as there are positives and negatives as we move into the final quarter of 2024. First, a rate-cutting cycle typically is a positive for the markets. As well, economic growth has persisted, with inflation seemingly back under control and labor market strength continuing. Companies are in good shape, and lower interest rates help ease balance sheet pressure. Equity market performance also broadened out this quarter. In other words, more companies besides the artificial intelligence ‘winners’ added to the positive market returns.

However, there are some persistent negatives. A soft landing is difficult to achieve, and the Fed is essentially navigating a high-wire act: cut rates too much, and inflation could take off again, or wait too long to cut, and the economy could fall into recession and labor markets could materially weaken. As well, as we get closer to November 5th, U.S. elections will continue to create volatility. Geopolitical tensions, particularly in the Middle East, have worsened. And on the individual company level, the financial markets have dealt harshly with disappointments, as worse-than-expected earnings results have resulted in major stock declines.

What Could Derail the Rally?

Despite some ups and downs along the way, equity markets are at record highs. We’re in a period of exuberance, disguised by the fact that it feels gloomy and unstable. It’s healthy to wonder if there are risks building beneath the surface. Remember we had a long period of low interest rates before the Fed began to rapidly increase rates in 2022 to contain rapidly rising inflation. In an artificially low-rate environment, financial discipline can weaken as investors chase the same or higher returns by taking more risk. The low rates and stock market strength also created a bonanza for private equity and private credit markets, as large institutions shifted their investment allocations to higher-yielding, higher-risk asset classes to meet their hurdle rates. Private equity saw exponential growth – in 2022 private market assets under management had grown to $9.7 trillion from $600 million in 2000[1]. There has been a wall of money competing for private companies. In addition, housing dynamics remain unusual. Low inventory and low mobility (as homeowners with very low mortgages sensibly stay put) have continued to support high housing prices. Higher mortgage rates have added to the lack of affordability.

Despite this backdrop, the rapid spike in the Fed Funds rate beginning in 2022 has thus far caused limited corporate and economic impact. We did have a few banks fail, but ultimately there was less fallout than expected from the rate increase. Now, we are back in a rate-cutting cycle, which is typically a positive for market returns. Corporate earnings, a major engine behind the financial markets, have remained strong.

Outlook

Given how strong the markets have been, it would be unsurprising to have some profit-taking and periods of correction, particularly leading up to the elections. Rising geopolitical tensions could add additional negative sentiment to the markets. There are numerous trip wires to be aware of, including a potential recession, a blow-up in the unregulated private markets and a correction in the housing markets. Markets have reached record levels, so there is limited room for error. Longer term, risk and return appear more balanced. The Fed cutting rates should set us on a path to monetary policy “normalization”, while global central bank easing and continued corporate earnings growth should continue to at least support markets. While future returns may be more muted, as always, maintaining a diversified, balanced portfolio of high-quality companies remains the key to long-term wealth management.

[1] https://www.hamiltonlane.com/en-us/insight/truths-revealed/private-markets-today

Lariat Wealth Management is a registered investment adviser offering advisory services in the State of Colorado and other jurisdictions where exempted. Registration does not imply a certain level of skill or training.

This publication is for informational purposes only and should not be relied upon as the sole factor in an investment making decision. Past performance is no indication of future results. Investment in securities involves significant risk and has the potential for partial or complete loss of funds invested. Lariat Wealth Management does not warrant that the information will be free from error. The information should not be relied upon for purposes of transacting securities or other investments. Your use of the information is at your sole risk.

.