Markets powered higher in the third quarter of 2025 and are up significantly since the April 2025 Liberation Day lows. Since the recent market lows in October 2022, the S&P 500 is up nearly 90%[1]. The S&P, Nasdaq and Dow stock market indices all hit all-time highs this quarter, driven by the likely beginning of an interest rate-cutting cycle by the Federal Reserve, continued investor exuberance around the potential of artificial intelligence, and economic strength. Are we overdue for a correction?

Fed Rate-Cutting, AI Momentum, Economic Resilience Drive Third Quarter Market Strength

Equity markets surged in the third quarter, driven by the following key themes:

- Interest rate cuts typically positive for the markets: The Federal Reserve cut the Fed Funds target rate by 25 basis points in September, in line with market expectations. Rate cuts boost economic activity by lowering borrowing costs and provide a positive backdrop for the markets, particularly if there is no economic or financial market distress. Two more 25 bps cuts are anticipated by year-end.

- Artificial intelligence excitement accelerating: Optimism about the potential of artificial intelligence continued in the third quarter. Large technology companies including Google, Meta, Microsoft and OpenAI continue to spend hundreds of billions on the infrastructure necessary for AI.

- U.S. economy remains strong: Despite the noise, tariffs so far have had only a limited impact on inflation, corporate earnings and the overall economy. Many companies have been negatively impacted, however there has not been an overall material negative effect yet as companies have worked through pre-tariff inventories, have raised prices, and/or have simply absorbed the hit to profits. The key question is whether or not there will be an impact and if we are just in a temporary lag period before there are material repercussions.

- Corporate profits remain strong: The estimated growth rate for year-over-year earnings for the third quarter (reports will be coming out over the next few months) is 8%[2]. That rate would mark 9 quarters of earnings growth for the S&P 500 Index and follow on Q2’s 13% growth. Note that the information technology sector is driving a large amount of this expected growth.

- International strength: Financial markets outside of the U.S. have surged this year. The EAFE index, a stock market index which tracks large and mid-sized companies in developed countries outside the U.S. is up 26%[3], helped by significant U.S. dollar depreciation and new investment themes (European aerospace & defense, Japanese activism) .

Major Financial Market Returns

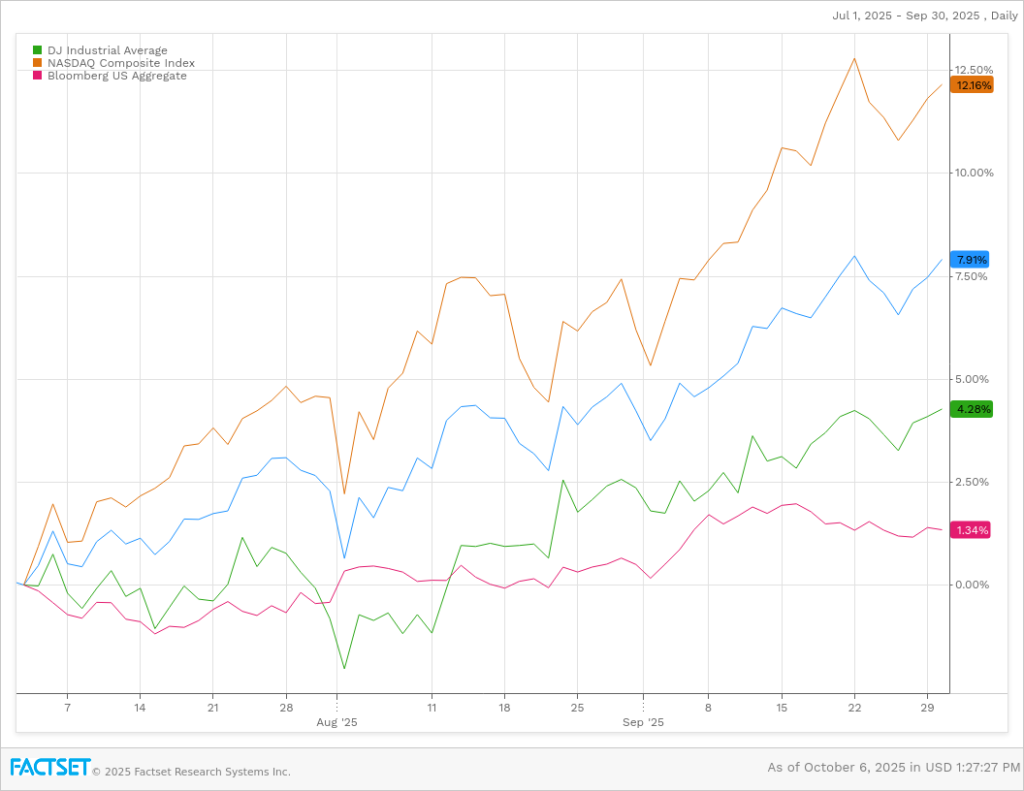

In the third quarter of 2025, the S&P 500 Index, a market-capitalization weighted index which tracks 500 leading U.S. companies, increased nearly 8%. The NASDAQ Index, which tracks stocks listed on the NASDAQ and tends to be tech company-heavy, increased over 12% and the Dow Jones Industrial Average, which tracks 30 mature, strong companies, was up over 4% in the third quarter of 2025. Om fixed income markets, the Barclays U.S. Aggregate Bond Index increased over 1% during the quarter.

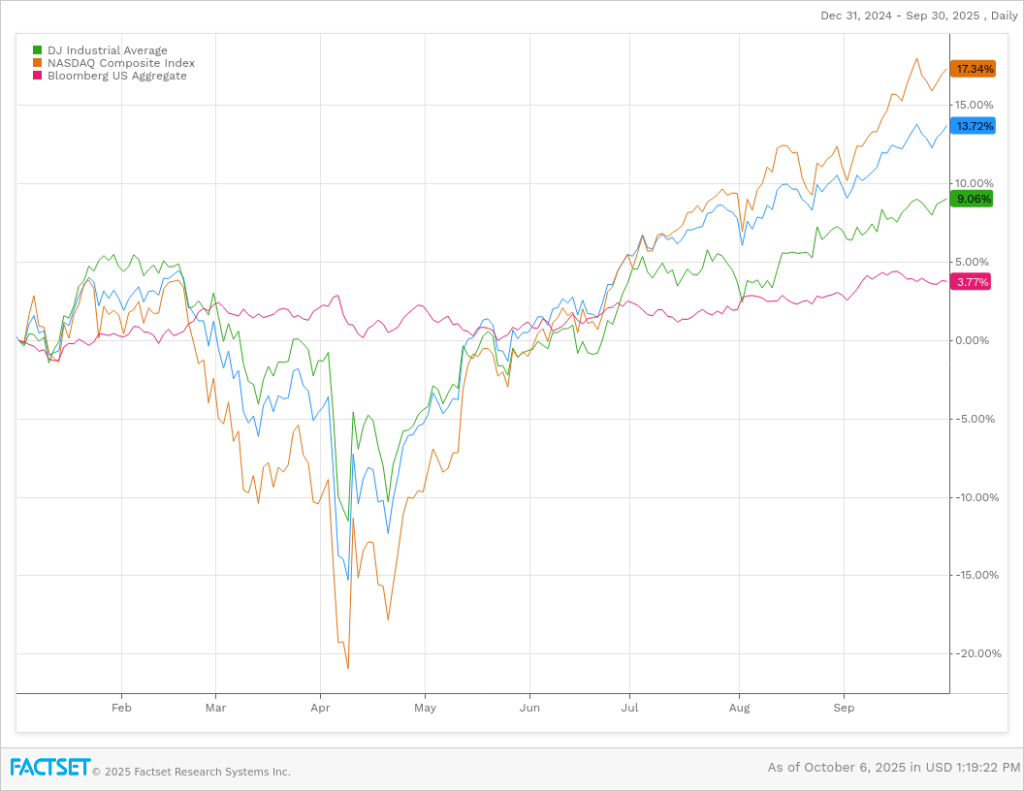

Year-to-date through the end of the third quarter, the S&P 500 Index increased over 13%. The NASDAQ Index, was up nearly 17%, and the Dow Jones Industrial Average, was up nearly 9%. In fixed income, the Barclays U.S. Aggregate Bond Index is up nearly 4%.

Outlook: Risks Remain, FOMO Markets Looking Past Them

There are many positive aspects of today’s market environment. Short-term interest rate cuts by the Federal Reserve typically boost economic and financial market activity. Artificial intelligence could add significantly to economic productivity, corporate revenue growth and profit margins. And while the labor markets are weaker, they are holding steady at a “low-hire, low-fire” level.

However, this type of momentum, “fear of missing out” (FOMO) market sentiment can change on a dime. Real risks remain, and the following could trip market dynamics up as we move into the fourth quarter of 2025 and 2026:

- Market concentration and AI risk: The top 10 companies in the S&P 500 index make up over 40% of its market cap, the highest concentration we have seen in this index. Nearly all of these companies are highly exposed to artificial intelligence and the current infrastructure spending boom. Should this slow, these top companies may correct and pull down the S&P 500 Index overall.

- Higher relative valuations: The U.S. market’s forward P/E (price to earnings ratio, or in other words how much the market will pay for a company’s future earnings) is currently 22.8x[4] vs a 30-year average of 17x. When valuations are higher, there is less margin of safety for a stock’s price, and negative news can cause a stock price correction.

- Investor complacency: Financial markets have shrugged off quite a bit of negative news flow, including slowing labor markets, the risk of higher inflation, the U.S. government shutdown and increasing geopolitical risk. Ignoring increasing risk levels can increase the potential of a sudden negative reaction should the complacency suddenly end.

- Fed Policy Error Risk: The Fed has a dual mandate assigned by Congress to ensure price stability (ie, control inflation) and maximum employment. Typically, the Fed raises interest rates to control inflation, and lowers them to boost the economy and employment. In some cases the Fed’s dual mandate creates the risk that they make a policy error: what should they do if inflation is rising and the labor marketing is weakening? That creates a situation with two opposite policy responses, and increases the risk that the Fed makes the wrong move.

Holding a diversified portfolio of high-quality securities remains the cornerstone of long-term investment success. However long this bull market lasts, a downturn will come at some point. While unsettling, downturns are a normal feature of the financial markets. Understanding market dynamics and what could spark market downturns is helpful, and staying invested and adding to portfolios during times of weakness remains critical to long-term investment success.

[1] https://www.morganstanley.com/insights/articles/ai-spending-bull-market-2025

[2] Factset Earnings Insight, 10/3/2025

[3] https://www.msci.com/indexes/group/developed-markets-indexes#msci-world-index

[4] J.P. Morgan Guide to the Markets, 9/30/25

This communication is for informational purposes only. Investment in securities involves significant risk and has the potential for partial or complete loss of funds invested. This publication is not intended as an offer or solicitation of an offer to buy or sell, or as an endorsement of any company, security, fund, or other securities or non-securities offering. This publication should not be relied upon as the sole factor in an investment making decision. Past performance is no indication of future results.