As 2026 began, investors had profited from three years of strong equity market returns and were cautiously optimistic about the market’s outlook for the year. Market-supportive Federal Reserve rate cuts were expected to continue, despite increasing levels of worry over the level of AI investment spending. Equity markets were relatively resilient through the middle of the quarter. Suddenly, companies perceived to be at risk of AI disruption saw rapid declines. Then, at the end of February, the Iran war began, disrupting oil supplies from the Middle East, driving oil prices up and raising concerns of inflation, rate hikes and risks to growth. The markets are easily spooked, and uncertainty overall has increased.

Q1 2026: Key Points

- After strong market performance for the past three years, 2026 year started with a more mixed outlook.

- At the beginning of Q1 2026, investors were focused on the AI spending boom and potential interest rate cuts by the Fed.

- Companies perceived to be vulnerable to AI disruption, including software, transportation and financial data, sold off dramatically.

- This selloff caused anxiety for investors in private credit, which are loans provided by non-bank lenders. Redemptions, or requests for the return of investment, surged.

- At the end of February, the U.S. and Israel initiated a joint military operation attacking Iran, resulting in oil supply disruption through the Strait of Hormuz and surge in oil prices.

- Expectations for a cut in short-term interest rates now off the table – Fed to take a “wait-and-see”[1] approach to impact of war.

Q1 2026: Market Performance

The equity markets posted a down quarter after double-digit market returns in 2023, 2024, and 2025. The S&P Index fell nearly -5% in the first quarter of 2026. The NASDAQ index fell by over -7%, and the DJIA fell nearly -4%. The market reaction to the strikes on Iran and beginning of the Iran war was similar to that of the announcement of the Liberation Day tariffs nearly a year ago, with a sharp market selloff and subsequent slight recovery to close the quarter.

Source: Factset

AI: Still Driving the Market, But Skepticism Is Increasing

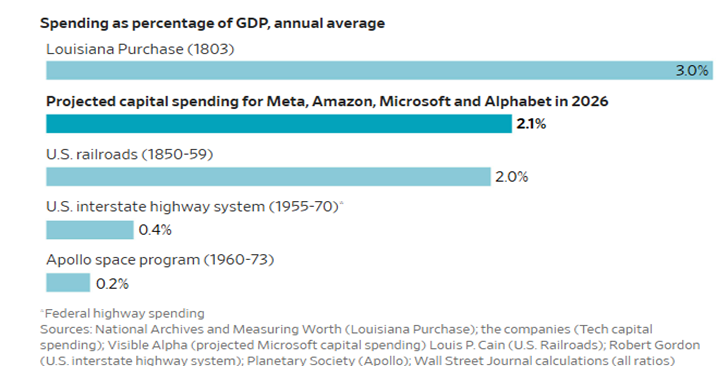

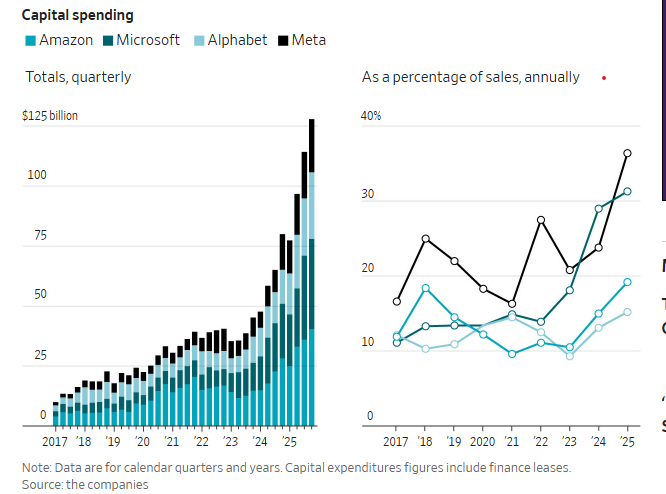

Massive Investment in AI: The top five “hyperscalers”(Google, Meta/Facebook, Microsoft, Amazon, Oracle), are expected to spend nearly $700bn in 2026[2], a meaningful year-over-year acceleration from already high levels. This investment includes spending on the necessary chips, major data center buildouts, and AI-specialized personnel.

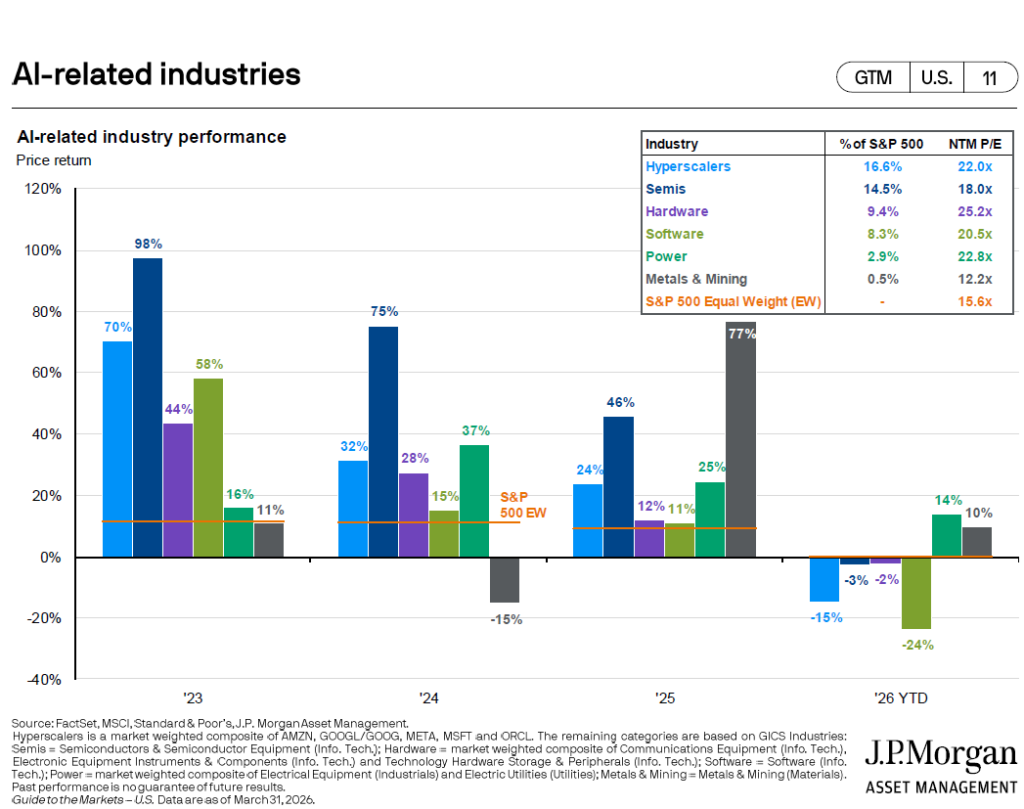

AI is Driving Market Performance: The overall impact of AI investment on the markets overall is significant. The tech and adjacent interactive media sector drove 65% of the market’s earnings growth over the past two years and about a third of real GDP growth[3]. The market’s large-cap “Magnificent 7” (Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia and Tesla) companies are AI companies. They now account for a major portion of the market’s return and are ~1/3 of the S&P 500 index. As goes AI, goes the market overall.

Investor Skepticism Increasing: As more money pours into these investments, the timing and magnitude of the profits companies make on AI has been questioned. Investors have also started to worry that the business models for these leading companies are changing, potentially permanently, as they shift more and more of their significant annual cash flow to fund AI investments.

AI Disruption Causing Selloffs: Late 2025 and early 2026 brought the first major disruptions from AI. Companies, including software stocks, transportation logistics, financial data and commercial real estate, which were judged as vulnerable to AI and sold off sharply, in some cases on rumor alone.

Source: JP Morgan Asset Management, Guide to the Markets, As of March 31, 2026

Ripple Effect of AI Disruption Into Private Credit: Private credit is lending provided by institutions that are not banks, and can be higher risk than regulated bank lending. Private credit lenders had large amounts of exposure to software companies in their portfolios. Investors rushed for the exits, concerned about the potential for defaults in these businesses. At present, the consensus view is that private credit’s issues are not systemic, but it is worth closely monitoring.

AI Opportunity is Real: Note that this is not a doom-and-gloom view of AI. Early use cases have emerged, beyond simply asking ChatGPT a question or simplistic data insights. Many companies are likely to see material efficiencies and productivity enhancements, and could benefit from revenue acceleration and margin expansion. A new technological network is being built out – just as railroads, telecom and the internet were. These new networks precipitated change and brought great opportunity.

The Federal Reserve Goes Into “Wait-and-See” Mode

Early 2026 Market Expectations Were For More Rate Cuts: At the beginning of 2026 market participants expected .25-.5% additional cuts to the Federal Fund rate, which would have continued the rate-cutting cycle which started in 2024. The Fed has held rates steady so far in 2026.

Dual Mandate – What’s the Fed to Do? Remember the Fed has a “dual mandate”, namely, it must support employment and also maintain price stability (i.e., keep inflation in check). Those goals can be at odds, and prompt different interest rate actions. The data the Fed reviews has been complicated by the effects of AI on the labor market, lack of data from the government shutdown and now, the Iran war.

Iran War Clouds Outlook: The recent attack on Iran and disruption to oil in the region caused the price of oil to increase rapidly. It is a short-term price shock, but the longer the war persists the risk of inflation increases. This uncertainty resulted in changed expectations of a future Fed move from rate cuts to no action, or even a potential rate hike and the resulting deceleration of the economy. The Fed is now in “wait-and-see” mode, and rate cuts are no longer baked into market expectations for 2026. The risk of a rate hike and slower growth has increased.

2026 Outlook: The Iran War Increases Downside Market Risk

The outlook for 2026 was mixed to positive at the beginning of the year. The Iran war increases uncertainty and raises risks to the downside. Should the conflict resolve quickly, and the oil price shock actually prove temporary, the markets will respond positively. Rate cuts would boost the market recovery.

The key items to watch as we move through the year include:

- The magnitude and duration of the Iran war, which will affect oil prices, inflation and the federal budget deficit

- Inflation and labor market data and the future path of Fed interest rates and monetary policy

- Key players in the artificial intelligence race – when will we see AI-related profits from AI companies? What about productivity benefits to profit margins?

- Will private credit’s challenges cause a broader impact on the financial system?

- Expect political noise to increase even more as we approach mid-term elections.

Risk and uncertainty increased this quarter. Market declines are never comfortable but are a part of investing, and investors must weather the declines to benefit from long-term gains. It is a roller coaster, not a straight line up and to the right. As always, a portfolio of high-quality securities remains the cornerstone of long-term investment success, through ups and downs.

This material has been prepared for informational purposes only. All opinions and estimates constitute the firm’s judgment as of the date of this publication and are subject to change without notice. This material is not intended to provide, and should not be relied on for tax, legal or accounting advice. It is not intended as an offer or solicitation with respect to the purchase or sale of any security. Investing may involve risk including loss of principal. Past performance is no guarantee of future results.

[1] https://news.harvard.edu/gazette/story/2026/04/powell-issues-a-warning-on-u-s-debt/

[2] https://www.cnbc.com/2026/02/06/google-microsoft-meta-amazon-ai-cash.html

[3] Empirical Research, Portfolio Strategy 2026, AI and Everything Else, March 26, 2026